Diagnostic studies for SDG innovation - Dutch Ministries of Foreign Affairs and the Economy. 2012-2013

Design planning and front-end inquiry for informal trade development in East African Community

Winner of iBoP Asia Small Grant Competition 2008 for developing front-end inquiry on informal economy systems

Redesign of systems to improve the student UX from admissions inquiry to job placement. Director, Graduate Admissions & Student Services. 2002-2005

Participatory research to inform service design strategy for rural solar hybrid minigrids

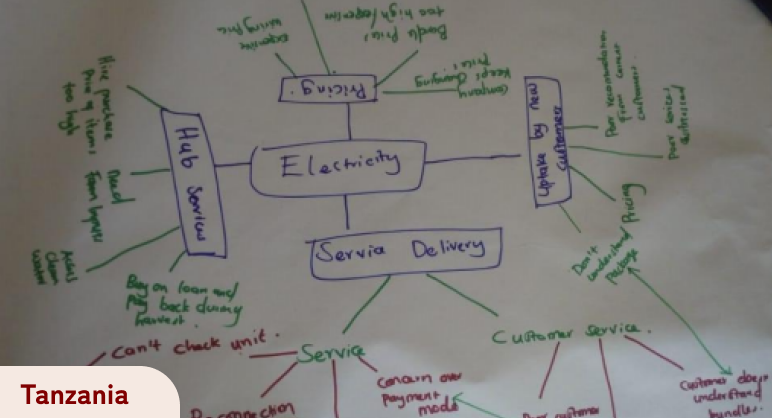

Off-grid energy consumption behaviour study to inform market development strategy for renewable energy

Between 2014 -2019, primary research to inform product development strategy for Africa-focused startups

Exploratory market assessment for informal cyber cafe industry of Kenya to inform marketing & pricing strategy

Collaboration with Veryday, Stockholm for Vodafone Concept Design Group, Dusseldorf

2008 Exploratory user research among the lower 75% of population by income for mobile phone design planning

Contribution of 5Ds framework for inclusive business & tools for business model design

Digital Financial Literacy programme design & Train the Trainer handbook for pilot

Rapid response social design innovation intervention for last mile urban food security (funder: Urgent Action Fund Kenya)

Prototyped in Kenya, and tested in Benin. Low-literacy & No-literacy financial planning tools.

October 2015 Opening Keynote & venture design coach for young Francophone West African entrepreneurs

2004-2010 Numerous projects with cofounders including Founding Editor, Core77/BusinessWeek Design Directory

2005 On half year retainer for internal market development strategy

2005-2006 Consultant

2006 Two separate white papers identifying opportunities in India and China emerging creative economy

1991-1994 Design Services Market Development